10 Simple Techniques For Paul B Insurance

The Main Principles Of Paul B Insurance

The thought is that the cash paid out in insurance claims over time will certainly be much less than the total premiums collected. You may seem like you're throwing cash gone if you never submit a case, but having item of mind that you're covered in the occasion that you do endure a substantial loss, can be worth its weight in gold.

Envision you pay $500 a year to insure your $200,000 home. You have ten years of paying, and also you've made no cases. That comes out to $500 times one decade. This means you have actually paid $5,000 for home insurance policy. You start to question why you are paying so a lot for absolutely nothing.

Due to the fact that insurance policy is based upon spreading out the risk amongst lots of people, it is the pooled cash of all individuals paying for it that enables the business to build assets and also cover claims when they take place. Insurance coverage is a business. Although it would certainly behave for the companies to simply leave rates at the exact same degree regularly, the truth is that they need to make sufficient money to cover all the prospective claims their insurance holders may make.

The Best Strategy To Use For Paul B Insurance

Underwriting adjustments and also price boosts or reductions are based on outcomes the insurance policy firm had in past years. They sell insurance policy from only one business.

The frontline individuals you take care of when you purchase your insurance are the agents important site and brokers who stand for the insurance provider. They will discuss the see kind of products they have. The captive representative is an agent of only one insurance provider. They an accustomed to that business's items or offerings, however can not talk in the direction of various other firms' plans, rates, or item offerings.

They will have access to even more than one firm and also have to understand regarding the range of items supplied by all the firms they represent. There are a few vital inquiries you can ask yourself that could assist you decide what kind of coverage you require. Exactly how much risk or loss of cash can you presume by yourself? Do you have the cash to cover your costs or financial debts if you have a mishap? What concerning if your house or car is ruined? Do you have the savings to cover you if you can not function due to a mishap or illness? Can you manage greater deductibles in order to decrease your expenses? Do you have special demands in your life that require additional protection? What concerns you most? Plans can be customized to your requirements and also identify what you are most anxious about shielding.

The 45-Second Trick For Paul B Insurance

The insurance coverage you need differs based on where you are at in your life, what type of possessions you have, and also what your long term objectives and tasks are. That's why it is crucial to take the time to discuss what you want out of your policy with your agent.

If you secure a funding to buy an auto, as well as after that something occurs to the cars and truck, gap insurance coverage will certainly repay any type of section of your lending that conventional vehicle insurance doesn't cover. Some lenders need their debtors to lug void insurance policy.

The main purpose of life insurance coverage is to offer money for your recipients when you pass away. Depending on the type of plan you have, life insurance policy can cover: Natural fatalities.

Not known Factual Statements About Paul B Insurance

Life insurance coverage covers the life of the guaranteed person. Term life insurance policy covers you for a period of time picked at purchase, such as 10, 20 or 30 years.

If you do not pass away throughout that time, no one earns money. Term life is prominent because it supplies big payments at a lower expense than long-term life. It likewise supplies protection for an established number of years. There are some variations of common term life insurance policies. Exchangeable plans allow you to transform them to long-term life plans at a higher premium, enabling for longer and possibly much more adaptable protection.

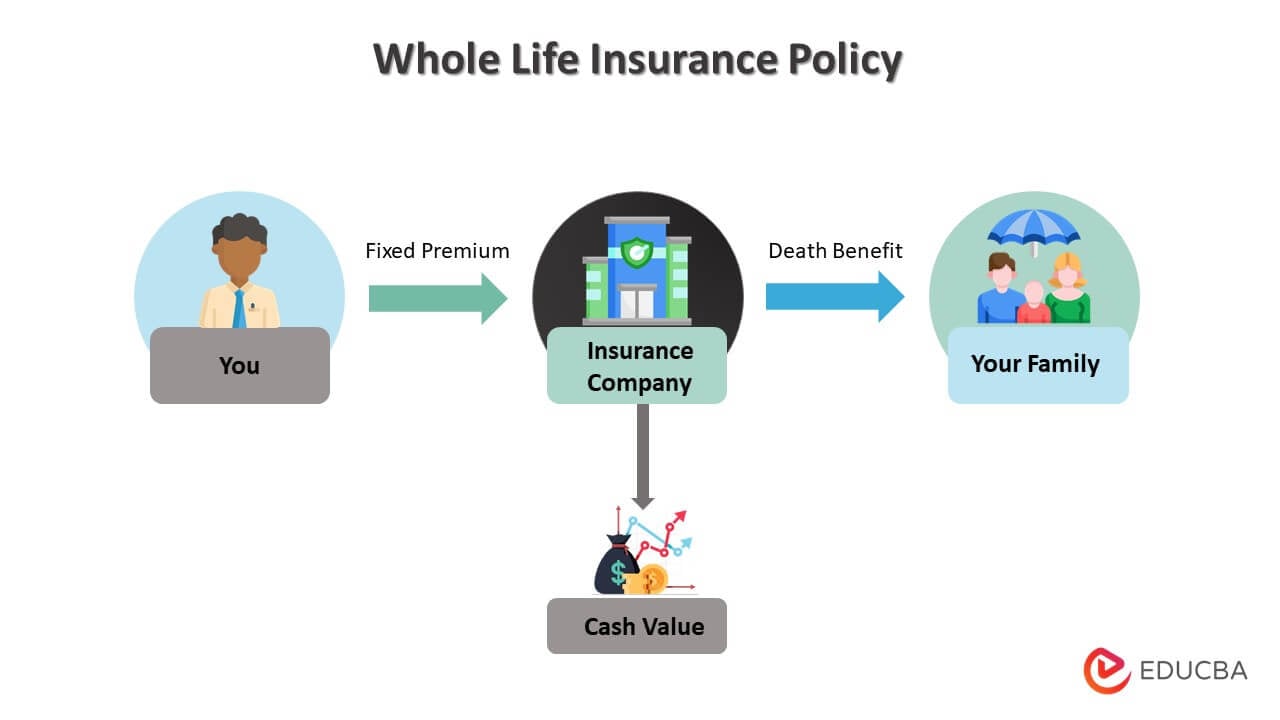

Permanent life insurance policy policies construct cash worth as they age. The cash money worth of whole life insurance policies grows at a fixed price, while the cash worth within universal plans can rise and fall.

Paul B Insurance Fundamentals Explained

If blog you compare ordinary life insurance policy rates, you can see the distinction. For example, $500,000 of whole life insurance coverage for a healthy and balanced 30-year-old woman prices around $4,015 yearly, usually. That very same degree of protection with a 20-year term life policy would cost approximately regarding $188 every year, according to Quotacy, a brokerage firm.

Those financial investments come with even more threat. Variable life is one more irreversible life insurance policy option. It sounds a whole lot like variable universal life however is in fact different. It's an alternate to whole life with a fixed payout. Insurance holders can make use of financial investment subaccounts to expand the cash money worth of the policy.

Here are some life insurance policy basics to assist you better comprehend exactly how protection functions. Costs are the settlements you make to the insurance provider. For term life policies, these cover the price of your insurance policy and also management costs. With a long-term policy, you'll also be able to pay money right into a cash-value account.